It’s often thought that investing in property is always a good thing – “as safe as houses” as the saying goes. But not every property necessarily brings in the returns an investor is looking for.

Sometimes, it might be necessary to ditch a property that’s looking like a lemon.

Just what is an under-performing property?

A property might be an under-performer if it doesn’t meet the goals you have set or perform as you had hoped.

For example, the value of the property might not be growing in line with the median increases for the suburb.

There could be several reasons for this:

- You paid more for a property than you should have, and its value is not increasing – or at least not yet.

- You bought in the wrong location for your desired capital growth.

- You invested in an older property only to discover it needs a lot of costly improvements or repairs to be viable.

- You bought property in a mining town where prices were high during a boom period, but have since plummeted.

- You invested in a high-density off-the-plan apartment, and other apartment blocks being built in the adjoining streets are affecting its value.

- You purchased a house and land package in a new estate where there is an abundance of new land releases, therefore reducing the scarcity factor.

Deciding whether to sell or to wait

So how do you decide whether to pull the pin and cut your losses now, or hang on and hope for future growth? After all, it might be that in time the property does increase in value. On the other hand, it might be better to sell it and invest in a better performer.

There is a lot to think about when you are in this position, and you will need to ask yourself several questions:

- Is capital growth likely to happen in the next few years? If not, would some improvements be worth doing to increase its growth potential?

- Are there any major developments or zoning changes anticipated that could influence property prices in the area? What happens if another development pops up next to yours, will it restrict your views?

- Is this an appropriate time to sell? For instance, if the current market is flat, it might be worth waiting. On the other hand, the longer you hang on to a low-quality investment, the more it is going to cost you.

- Would you be better off selling and investing your money into something more promising, even if it means taking a loss and incurring some costs?

To answer these questions, you will need to do your sums and speak to experts such as your banker or mortgage broker, accountant and financial planner. You’ll need to consider what it cost to buy the property in the first place and what its current market value is, and whether what will be left after repaying the loan (if anything!) is worth investing elsewhere. On the other hand, if a loss is incurred from the sale, you might be able to use it to offset future capital gains and tax liabilities.

Calculation example

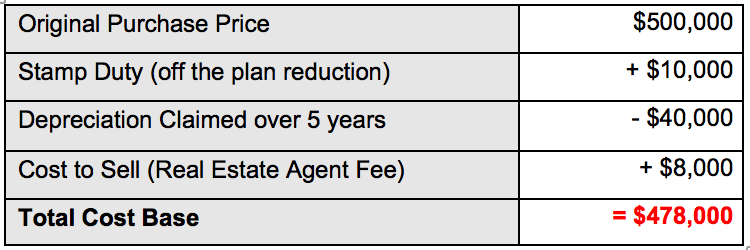

Let’s say you purchased an apartment off-the-plan five years ago for $500,000.

Unfortunately, this property has not performed well in terms of capital growth and at current market value is still worth $500,000, so now you are thinking of selling.

So how might the figures look in our scenario?

Calculate Cost Base of Selling Property for Tax Purposes

Interestingly, even though the property value has not increased if you have held the property for over 12 months (in this scenario 5 years) you have a capital gain of $22,000 because you have depreciated the property along the way. A capital gain of $22,000 is then discounted by 50% (current tax law) to $11,000. The worst case scenario is if you are a high-income earner on the highest marginal rate the tax owed would be $5,170.

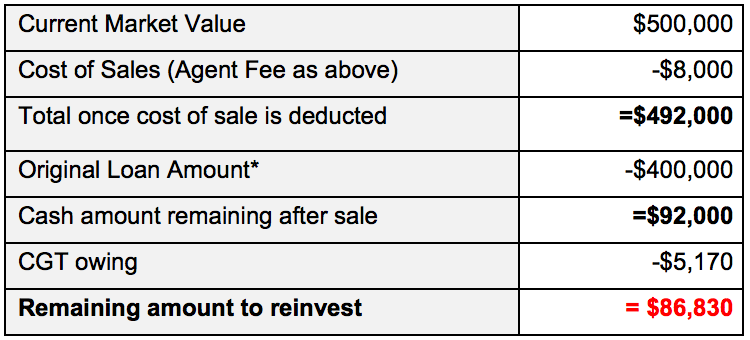

Net Cash Position Post Sale

*80% of original amount borrowed, interest only loan type

Based on this example, you would have $86,830 to invest in another property. Even if you borrowed more than 80% of a higher quality $500,000 investment property, you may still have the ability to recoup your losses and achieve better potential for returns over the medium to long-term.

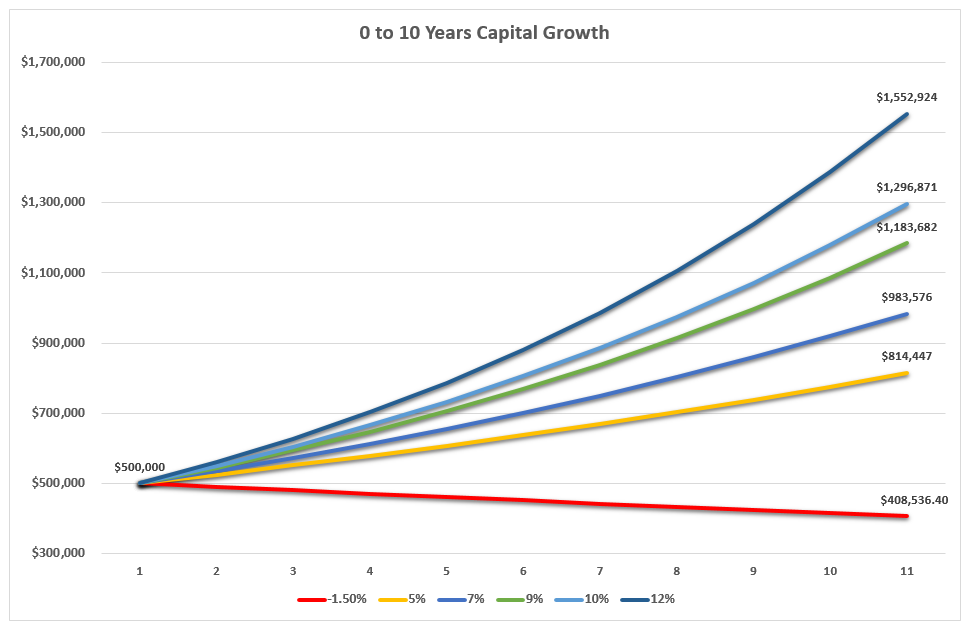

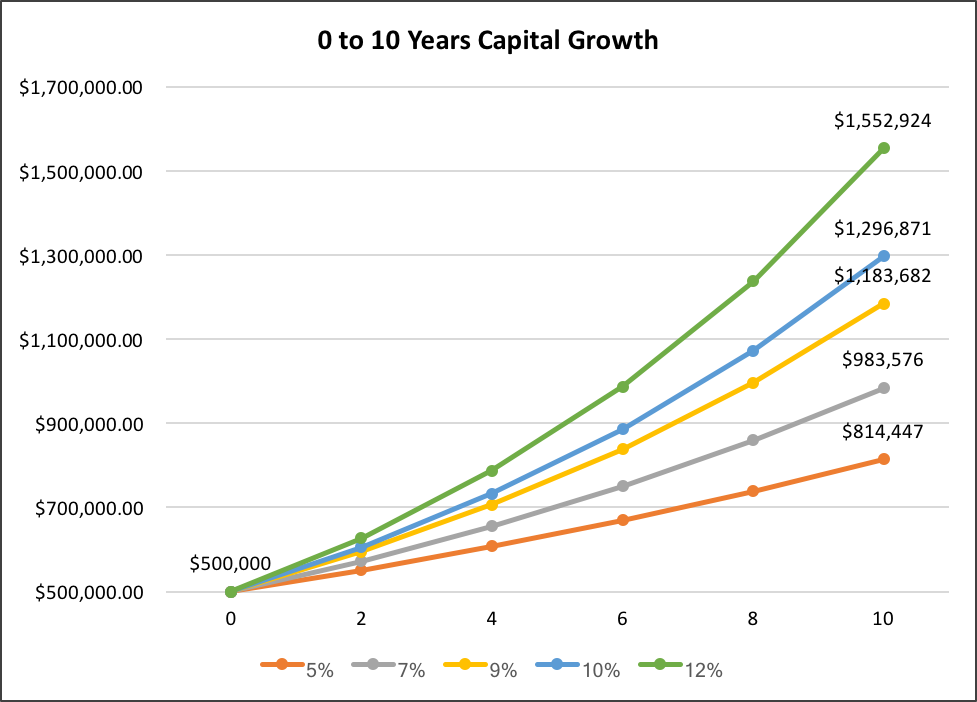

As demonstrated in the table below, reinvesting your dollars into an asset that grows will reward you in the longer term.

However, if the properties in your portfolio have fixed loans in place, the break costs may be too high, and if your loans are cross-collateralised against another house, you will need to factor this into your loan restructuring.

Seek professional assistance

In some cases, selling the property might be a no-brainer, whereas in others the answer might be more complex.

Before making a final decision, it’s important to speak to your accountant so that they can model your scenario based on your tax position. Your banker or mortgage broker can also advise on your existing loan structure, and what effect it could have if you close the loans (cross-collateralised, fixed loan break costs etc). They should also run serviceability calculations on your proposed future purchase.

You might also want to consider talking with a buyer advocate. A professional advocate can provide an expert opinion on the quality of your property and the current market conditions. They can also give you recommendations if you decide to sell and invest elsewhere.

Buying and selling property can be complex business, so make sure to get the professional advice you need before pulling the plug on your investment!