The May 12, 2026 Federal Budget has announced sweeping reforms to property investment tax, targeting both negative gearing and Capital Gains Tax (CGT).

Set to begin July 1, 2027 these changes have introduced uncertainty into the market. Leaving many to question if property can remain a cornerstone of a successful investment strategy.

To answer that question, you need to understand the new landscape and the potential impact on your finances today and in the future.

The following section examines the proposed changes and their implications for investors across both new and established properties. It helps to provide a framework for assessing your investment strategy for the years ahead.

Grandfathering & Transition Period

This blog focuses on the purchasing of established or new properties under the proposed changes.

However, for existing owners all properties held at the time of the Federal Budget announcement (including where a contract has been entered into,but not yet settled) can negatively geared in future years until sold. Existing properties purchased between budget night and the 30 June 2027 can be negatively geared during the transition period. And then from 1 July 2027 they can carry losses forward only.

There will be no change in CGT arrangements for assets purchased and sold prior to 1 July 2027. Assets owned prior to 1 July 2027 and sold after will use a hybrid model to calculate your capital gains tax owing. The 50 per cent CGT discount will apply to the property’s value at 1 July 2027 and then it will switch to the indexation model for future calculations.

Negative Gearing

What Is Changing?

Negative gearing is a tax strategy where an investor’s expenses on a rental property, including loan interest, exceed the income it generates. This creates a net rental loss, which investors could previously deduct from their other taxable income, such as their salary. This reduced their overall tax liability for the year.

The 2026 Federal budget proposal significantly alters this mechanism. From 1 July 2027, the ability to claim negative gearing deductions against personal income will be limited to newly constructed residential properties only.

For investors purchasing established properties after this date, negative gearing as we know it will no longer be available. Net rental losses on established properties will no longer be offset against salary income. Instead, these losses must be carried forward to be offset against future rental profits from the same property or used to reduce the capital gain upon its eventual sale.

What this means for investors buying ‘Existing Properties’

The most immediate impact of the negative gearing changes will be on cash flow and loan servicablity.

The new carry-forward loss mechanism means that while the tax benefit is not lost entirely, it is deferred. Investors will need to fund the property’s shortfall out of their own pocket during the years it runs at a loss, without the immediate tax relief they previously enjoyed.

This changes the calculation for investors. The focus must shift from short-term tax reduction to long-term asset performance. The accumulated losses will reduce the taxable income when the property eventually becomes positively geared or when it is sold, which will decrease the final CGT liability. However, the holding costs in the interim will be higher. Investors considering established properties must now model their cash flow with precision, ensuring they have the financial capacity to service the asset without the immediate support of tax deductions against their wages.

What this means for investors buying ‘New Properties’

The intent of the government’s change in policy direction is to incentivise new home construction. Therefore, negative gearing will continue to be available for new properties.

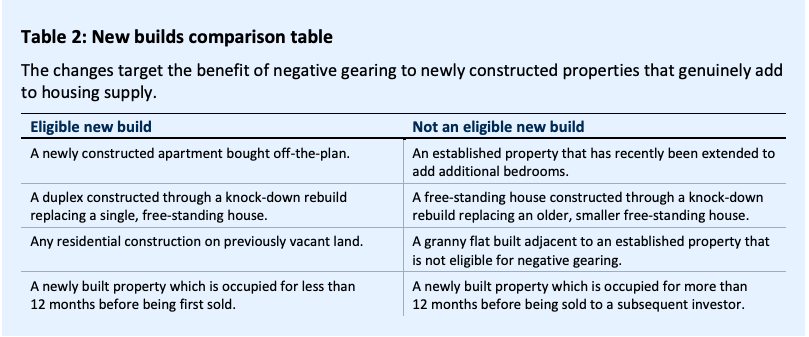

What is important is understanding the definition of a new property and ats its core a new property must add to supply.

The best place to find that answer is on Federal Government’s Budget 26-207 website. The below table from their website provides a good overview. Though we admit we still have some questions!!

Capital Gains Tax

What is changing

The second major reform involves Capital Gains Tax.

From 1 July 2027, the 50% CGT discount for individuals is replaced by a system of cost base indexation for assets held over 12 months. Instead of halving your gain, your property’s purchase price will be adjusted for inflation, and you will pay tax on the ‘real’ gain. Essentially each year you hold the property the inflation rate will be added to your purchase price (cost base).

A 30%* minimum tax will apply to net capital gains.

The question that everyone is asking is

Am I better off under the current (50%) discount model or the new indexation model?

And unfortunately (or fortunately!), there isn’t one answer.

The shift to the indexation model has several moving parts. Your income has always played a part but now years of ownership and the annual inflation rate have a significant impact of what you will take home after tax.

The indexation model could benefit long-term holders in high-growth markets but may increase the tax burden for shorter-term investors.

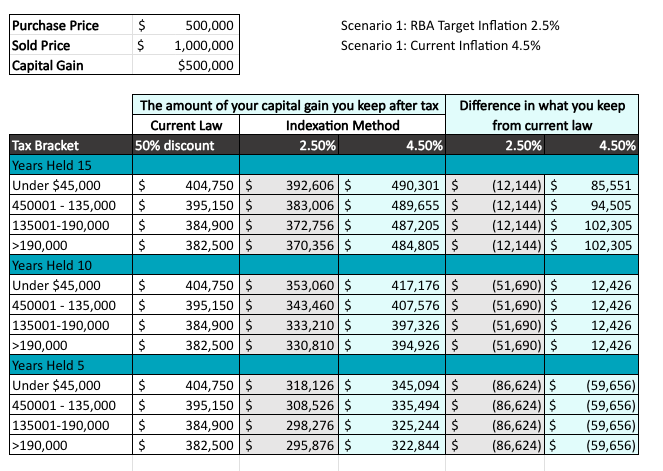

The table below models two scenarios illustrating the after-tax outcome on a $500,000 capital gain across varying hold periods and inflation rates. The minimum 30% tax rate has been applied throughout, and the inflation rate is held constant for each scenario. In practice, inflation will fluctuate year to year.

Which Capital Gains model are you better off under?

What this means for investors buying ‘Existing Properties’

The new arrangements will apply to capital gains that accrue after 1 July 2027 when they are realised. Individuals may pay more or less tax than under current settings depending on investment returns and inflation.

What this means for investors buying ‘New Properties’

Investors who buy new builds will be able to choose either the 50 per cent CGT discount or the indexation model.

Upon selling the property, they will have the option to choose the more favourable CGT calculation and pay the minimum tax when they sell.

So is investing in a property still a winner?

Yes.

Acknowledging the current pressures on the real estate market. Including cost-of-living increases and geopolitical instability, we maintain that the compounding growth of property over the long term remains a powerful vehicle for wealth creation.

However, success in this new landscape returns to a fundamental principle that our team and other experienced buyer’s agents have long advocated.

Your property selection is critical.

New builds have absolutely been incentivised with significant tax advantages. This does not, however, mean any new build constitutes a sound investment. From our analysis, the most promising opportunities will be in low to medium density new builds located in the middle-ring suburbs. Off-the-plan or high-density apartment projects continue to present a significant risk of poor capital growth.

For established properties, the loss of negative gearing will reduce cash flow and affect loan serviceability for some buyers. Interestingly, the Federal Government has shared data indicating that only a small percentage of tax filers, approximately 1%, currently use negative gearing as part of their wealth strategy.

We cannot stress enough the importance of running detailed calculations and financial scenarios to determine the optimal investment type for your specific circumstances.

Finally, it is important to remember that the Federal Budget must still pass through the Senate to be legislated. We expect considerable public and political discussion until the proposed changes are ratified. This uncertainty may cause some buyers to hesitate in the short term.

*Recipients of means-tested income support payments, such as the Age Pension or JobSeeker, will be exempted from the minimum tax if they receive any payment in the financial year in which they realise the capital gain.

Please note this article provides general information only. It will depend on your individual circumstances what strategy is best for you. The CGT calculation table numbers were sourced from this website: https://www.stockspot.com.au/cgt-calculator/

Contact Us

We’re happy to answer any questions you may have or you can simply request we catch up for a free, no obligation meeting to discuss your needs.